When hot works are undertaken during construction, insurers will expect that all ‘reasonable’ precautions are taken to prevent a claim from being made. However, this can be a grey area as there is no strict definition of the term ‘reasonable’.

Insurers normally have conditions specifically relating to the use of heat and could look to refuse payment of a claim if the hot works conditions are not strictly met and if they are relevant to the loss. These conditions vary from insurer to insurer, policy to policy and client to client. Below we will look at some examples of typical clauses which are applied to the different parties involved, the complexities of the claim process, risks of rejected claims, and how to overcome all of these issues by using Triflex cold liquid applied waterproofing:

Building owners policy

Application of heat

Within the building owners insurance policy there are common conditions concerning the application of heat for example:

- Where work of any nature or value whatsoever involves the application or generation of heat or sparks, the insured shall require a completed hot work permit from any workman or contractors undertaking the work and otherwise take such precautions as may be necessary to ensure a safe working environment having regard to the risk of fire;

- A copy of the completed Hot Work Permit must be retained for at least one month.

If there was a fire, failure to comply with these conditions would be relevant to the loss and non-compliance could, therefore, be used by insurers to refuse payment of the claim. The completion and retention of the hot works permit can be a considerable administrative task. The building owner would also need to have the requisite knowledge and experience to ensure a safe working environment having regard to the risk of fire, something which would likely require an internal Health and Safety risk assessment for all hot works.

Contractors policy

Hot works conditions

Similarly, construction contractors will have numerous clauses and conditions within their liability insurance that must be complied with concerning the use of hot works equipment. A fire occurring as a result of the use of any of this equipment would be relevant to the loss, and non-compliance could be used by insurers to refuse payment of the claim. Some examples of these clauses include:

- The area in which work is to be carried must be examined and combustible property within the vicinity of the work either removed or as far as practicable covered by non-combustible materials;

- Suitable fire extinguishing appliances to be kept available for immediate use at the point of work or as near as is practicable;

- Blow lamps, blowtorches and flame guns not to be lighted until required for use and extinguished immediately after use;

- Heating vessels to be kept in the open and not left unattended whilst in use;

- Gas cylinders not in use to be kept outside the building in which the work is taking place where practicable but in any event at least 15 metres from the point of application of the heat;

- Lighted torches and guns not to be left unattended;

- Hot air guns, hot air welders and strippers to be switched off when unattended;

- The insured shall arrange for a person who is competent in the use of fire extinguishing appliances to work in conjunction with the operative using the equipment to act as a fire watcher and to remain in attendance at all times until lighted flame equipment is extinguished;

- Upon completion of each period of work a thorough fire safety check to be made of the vicinity of the work. The fire safety check to be undertaken at regular intervals for a period of at least one hour after completion.

The claim chain

The claim chain will vary depending upon the contractual position and the form of contract.

For example, if the Building Owner has employed a Main Contractor who in turn employs a Roofing Company, who in turn employs a Self-Employed Roofer and assuming the Self-Employed Roofer is responsible for the fire and the building burns down:

- As far as the Building Owner is concerned their contract is with the Main Contractor and the Building Owner would claim via their insurance who would then approach the Main Contractor’s insurance;

- The Main Contractor’s insurance would then approach the Roofing Company’s insurance;

- The Roofing Company’s insurance would then approach the Self-Employed Roofer’s insurance.

If the Self-Employed Roofer’s insurance does not pay or has insufficient cover, the insurance of the Roofing Company should pay, if the Roofing Company’s insurance doesn’t pay, the Main Contractor’s insurance should pay and if the Main Contractor’s insurance does not pay, the Building Owner’s insurance should pay.

If a particular parties insurance does not pay, this does not absolve them of blame, as the insurance company up the line can sue those down the line, i.e. the Main Contractors insurer could sue the Roofing Company, who in turn could sue the Self-Employed Roofer.

This can be further complicated as certain JCT clauses give the Main Contractor the right to pursue the claim directly with the Self-Employed Roofer.

Summary

The net effect of the above is that all parties must:

- Understand and review the specific terms of their insurance policies;

- Take account of any changes in the conditions year on year;

- Understand the potential risks of hot works;

- Understand the potential financial risk of loss;

- Ensure that those employed under contract can demonstrate they have insurance in place and in a sum sufficient to cover the potential ultimate loss;

- Fully abide by the terms of their insurance;

- Take reasonable precautions to prevent loss.

Failure to do so could result in insurers rejecting claims, under insurance or the potential to be sued by the employer’s insurance for a contribution to the loss.

Given the magnitude of the potential loss as a result of fire and the prescriptive nature of the terms, any claim is likely to be both difficult and time-consuming to resolve and could lead to significant financial loss and even insolvency of those in the contractual chain. Given the potential risk, the only way to practically avoid issues is to avoid hot works.

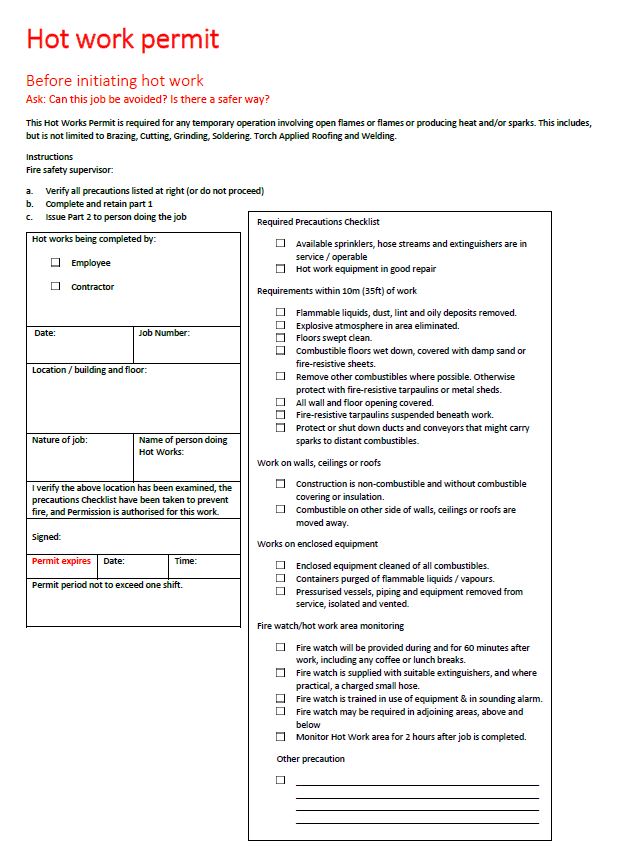

Furthermore, we discussed earlier within the Building Owner’s policy that a hot work permit is likely a requirement prior to completing any work involving heat or flames. This poses a key issue to the contractor, hot work permits commonly pose the question “Can this job be avoided? Is there a safer way?”.

That’s where Triflex systems and solutions come into their own. They are fully cold applied, avoiding any need for hot works. They can be applied all year round, and in temperatures down to 0°C and -5°C for details. In fact, we have been manufacturing these systems for more than 40 years and they have been installed around the world, proven and tested in some of the toughest environments.

Lastly, there is one further important factor for consideration. In addition to the insurance risk, hot works create a risk which under the principles of Health and Safety should be avoided where there is an alternative.

Triflex cold liquid applied waterproofing systems are the perfect alternative to traditional systems requiring the use of hot works.